Math and Money: Teaching Financial Literacy to Kids

Why Money Math Matters More Than You Think

Your child can solve 48 divided by 6, but can they figure out if they have enough allowance money saved up for that toy they want? Financial literacy for kids starts with the math they already know. The gap between classroom arithmetic and real-world money skills is smaller than most parents realize.

According to a report from the U.S. Joint Economic Committee, only 57% of American adults are considered financially literate. That number drops sharply among younger generations. The problem isn’t math ability. It’s that nobody connects the dots between what kids learn in school and how money actually works.

Research from the Cambridge University Press shows that money habits form as early as age 7. That means the window for building strong financial literacy for kids is right now, during the same years they’re learning addition, subtraction, and multiplication.

Starting with what they already know

Kids ages 5 to 7 are learning to count, add, and subtract. Those are the exact same skills they need to count coins, add up prices, and figure out change. You don’t need a special curriculum. You need a trip to the store.

Hand your child five euro coins and let them pick something at the bakery. Ask: “Do you have enough?” That single question activates addition, comparison, and subtraction all at once. It also teaches something textbooks can’t: the feeling of spending your own money.

For kids ages 8 to 10, the math gets more interesting. Multiplication lets them calculate how many weeks of allowance they need to save. Division helps them split a bill with siblings. Fractions come alive when you talk about sales: “This is 1/4 off the price. What does that mean?”

The Consumer Financial Protection Bureau recommends using everyday situations like these rather than abstract exercises. Their “Money as You Grow” guide breaks down age-appropriate money milestones that line up naturally with school math.

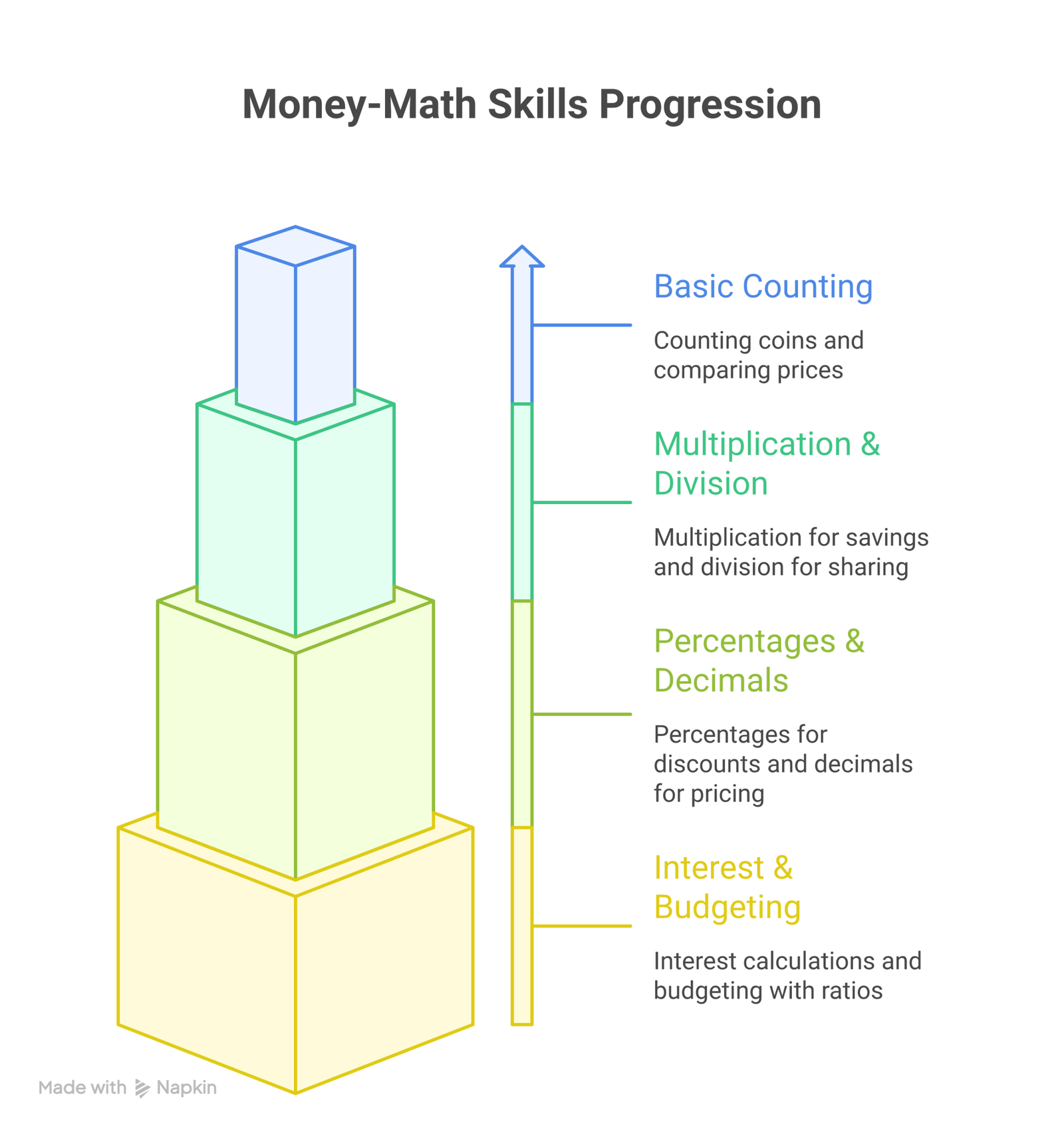

✓ Quick money-math connections by grade

- ✓ Grades 1-2: Counting coins, comparing prices, making change with addition and subtraction

- ✓ Grades 3-4: Multiplication for savings goals, division for fair sharing, basic budgeting

- ✓ Grades 5-6: Percentages for discounts and tax, decimals for exact pricing, fractions for proportional spending

- ✓ Grades 7-9: Interest calculations, budgeting with ratios, understanding debt and compound growth

The allowance experiment

Giving a child an allowance is one of the most effective financial literacy activities you can try at home. But the magic isn’t in the money itself. It’s in the math decisions that follow.

Say your child receives 5 euros per week. They want a game that costs 30 euros. Instead of telling them the answer, ask: “How many weeks will you need to save?” That’s division. Then ask: “What if you saved only 3 euros a week and spent the rest?” Now they’re comparing rates and timelines.

The American Psychological Association notes that children who practice making spending decisions develop better self-regulation. They learn delayed gratification through arithmetic, which is a skill that pays off long past childhood.

A simple tracking system works well here. A notebook or spreadsheet where your child logs income, spending, and balance. Each entry is a math problem: “I had 12 euros, spent 4.50, now I have…” That’s real subtraction with decimals, done by choice rather than assignment.

💡 The three-jar method

Give your child three jars labeled Spend, Save, and Share. Each week, they divide their allowance between the jars. This teaches fractions and percentages naturally. If they put 2 euros in Save, 2 in Spend, and 1 in Share, ask them what percentage goes to each jar. Suddenly, percentages make sense.

Grocery store math that actually works

The grocery store is the best free math classroom available to parents. Every aisle has problems to solve, and your child won’t even realize they’re practicing.

Start with price comparison. Two brands of cereal: one costs 3.20 euros for 500g, the other costs 4.80 euros for 750g. Which is the better deal? Your child needs division to find the price per gram, then comparison to decide. This is the kind of math that follows them into adulthood.

The National Center for Education Statistics reports that students who engage with applied math problems score higher on standardized tests than those who only do abstract exercises. Grocery math is applied math in its purest form.

Try giving your child a budget for a recipe. “We need ingredients for pancakes and we have 10 euros.” They’ll need to add prices as they shop, subtract from their budget, and make substitutions if something is too expensive. It’s problem-solving with real consequences, and they’ll remember it because the pancakes are at stake.

Teaching percentages through discounts and sales

Percentages are one of those topics that kids struggle with in textbooks but grasp quickly when money is involved. A “30% off” sign at the mall does more for percentage understanding than ten worksheet pages.

Walk your child through the calculation: “This shirt costs 25 euros and it’s 20% off. What’s 20% of 25?” They multiply 25 by 0.20 to get 5. Then subtract: 25 minus 5 equals 20. Done. They just used multiplication, decimal conversion, and subtraction in one real problem.

For older kids (grades 7-9), add tax into the equation. In Greece, the standard VAT rate is 24% according to the Independent Authority for Public Revenue (AADE). Ask your teen: “If something is listed at 40 euros before tax, what’s the final price?” That requires multiplying by 1.24, a real operation they’ll perform hundreds of times as adults.

The OECD’s Programme for International Student Assessment (PISA) includes financial literacy testing alongside math. Their findings consistently show that students who encounter math in financial contexts retain concepts longer and transfer skills more flexibly than those who learn through abstract problems alone.

Savings goals and the power of compound growth

Once your child understands basic saving, introduce the concept of interest. It doesn’t have to be complicated. You can play the role of “The Bank of Mom and Dad.”

Here’s how it works: offer to pay your child 10% interest per month on whatever they keep in their savings jar. If they have 10 euros at the start of the month, they earn 1 euro. Next month, they have 11 euros and earn 1.10. The month after that, 12.10 becomes 1.21 in interest. They’re learning compound growth without ever hearing the term.

According to Investopedia, compound interest is often called the most powerful force in finance. When your child sees their savings growing faster each month, the math becomes visceral. They feel multiplication working in their favor.

For older students, use a simple formula: A = P(1 + r)^n. Walk through it with real numbers. “If you save 100 euros at 5% annual interest, how much will you have in 10 years?” Pull out a calculator and watch their eyes widen at 162.89 euros. That’s the kind of math revelation that sticks.

📝 A word about debt

Once your child understands how interest helps their savings grow, flip the script. Show them that borrowing means interest works against them. If they “borrow” 10 euros from you at 10% monthly interest, they’ll owe 11 after one month and 12.10 after two. This is one of the most valuable math lessons you can teach, and it takes about five minutes.

Budgeting projects for different age groups

Budgeting is where all the math skills come together. The U.S. Department of the Treasury’s Financial Literacy and Education Commission recommends introducing budgeting concepts as early as age 8, using age-appropriate projects.

Ages 5-7: The lemonade stand budget. Give your child a pretend budget of 15 euros to run a lemonade stand. Lemons cost 3 euros, cups cost 2 euros, sugar costs 1.50. How much is left for a sign? Can they sell 20 cups at 0.50 euros each and make a profit? This is addition, subtraction, and multiplication rolled into a single fun project.

Ages 8-10: The birthday party planner. Give them a 50-euro budget to plan a birthday party. They need to allocate money for food, decorations, and a small activity. Let them research prices (you can help), create a list, and adjust when something doesn’t fit. Division helps when they need to figure out cost per guest.

Ages 11-14: The vacation researcher. Challenge your child to plan a weekend family trip on a fixed budget. They’ll need to compare hotel prices, estimate fuel costs (distance times price per liter divided by fuel efficiency), plan meals, and track running totals. This project touches on multiplication, division, percentages, and comparison, all driven by real motivation.

Tools like MathSpark can help reinforce the underlying math skills your child needs for these projects. MathSpark generates AI-powered math worksheets tailored to grades 1-9 in about 10 seconds, covering the specific operations (percentages, decimals, multi-digit multiplication) that budgeting requires. It follows the Pythagoras Exams methodology and covers the Greek school curriculum, so the practice connects directly to what your child learns in school.

Digital money and online math skills

Kids today grow up watching parents tap phones and cards to pay. Physical money is becoming less common, which creates a new challenge: how do you teach financial literacy for kids when money is invisible?

The Federal Reserve found that cash transactions account for less than 20% of all payments in the United States. In Europe, the trend is similar. For children, this means they need to understand numbers on screens, not just coins in pockets.

A digital spending tracker can help bridge this gap. Set up a simple spreadsheet with your child. Column A: date. Column B: what they bought. Column C: how much. Column D: running balance. Every entry requires subtraction, and reviewing the sheet weekly involves addition and comparison. It’s straightforward and builds the habit of tracking expenses.

For kids interested in tech, Khan Academy’s financial literacy course offers free video lessons that pair math concepts with money management. The course covers budgeting, interest, and investment basics in a format designed for younger learners.

Games that teach money math

Board games have been teaching financial literacy for over a century. Monopoly gets all the attention, but there are better options depending on your child’s age.

The Game of Life walks kids through career choices, salaries, and major purchases. Every turn involves addition and comparison. Payday focuses specifically on monthly budgeting, with players managing income, bills, and unexpected expenses. Both require ongoing mental math throughout the game.

For younger children, playing “shop” at home is hard to beat. Set up a pretend store with price tags. Give your child play money and let them buy items, count out payment, and calculate change. According to the National Association for the Education of Young Children, this kind of dramatic play supports mathematical thinking in ways that worksheets alone cannot.

Digital options exist too. Apps like Greenlight and FamZoo give kids debit cards with parental controls. Every transaction becomes a math conversation. “You spent 7.50 on a snack and had 25 euros. What’s your balance now?” The math is real because the money is real.

✓ Benefits of money-based math practice

- ✓ Makes abstract concepts like percentages and decimals concrete and memorable

- ✓ Builds real-world decision-making skills alongside arithmetic

- ✓ Develops patience and delayed gratification through savings goals

- ✓ Connects school math to adult life, increasing motivation to learn

- ✓ Creates natural conversation starters about values, priorities, and planning

Common mistakes parents make

The biggest mistake is avoiding money conversations entirely. A survey by T. Rowe Price found that 41% of parents feel uncomfortable talking about money with their kids. But silence doesn’t protect children from financial reality. It just leaves them unprepared.

Another common mistake is always bailing kids out. If your child spends their entire allowance on day one and has nothing left for the rest of the week, resist the urge to give them more. The discomfort of running out is the lesson. The math is clear: income minus spending equals zero, and zero means waiting until next week.

Some parents also make money conversations too serious or stressful. Kids pick up on financial anxiety fast. Keep the tone light and practical. Frame problems as puzzles to solve together, not tests to pass. The goal is building confidence with both math and money at the same time.

Finally, don’t skip the math step. It’s tempting to just tell your child the answer when they ask how much something costs or whether they can afford it. Instead, guide them through the calculation. “You have 8 euros and this costs 5.75. Can you figure out how much you’d have left?” That 30-second pause while they think is where the learning happens.

Building financial literacy for kids one math problem at a time

Financial literacy for kids isn’t a separate subject you need to squeeze into an already packed schedule. It’s math, applied to something your child cares about. Every allowance decision, every shopping trip, and every savings goal is a math lesson in disguise.

Start small. Let them pay for something themselves this week. Ask them to check whether a sale is actually a good deal. Have them track their spending for a month. These tiny actions build both mathematical fluency and financial confidence over time.

The Jump$tart Coalition for Personal Financial Literacy recommends starting as early as possible and building complexity gradually. That’s exactly how math works too. You wouldn’t teach algebra before addition. The same principle applies to money: start with counting coins, and by the time they’re teenagers, compound interest and budgeting will feel natural.

⚠️ Disclaimer

This article provides general educational guidance for parents as of March 2026. It is not professional financial advice. Every child learns at a different pace, so adapt the activities and concepts to your child’s age and readiness. When in doubt about age-appropriate financial topics, consult with your child’s teacher or a family counselor.

Frequently Asked Questions

At what age should I start teaching my child about money?

Research from Cambridge University suggests money habits begin forming around age 7. But simple activities like counting coins and playing shop can start as early as age 4 or 5. The key is matching the activity to your child’s current math level.

How much allowance should I give my child?

A common guideline is 0.50 to 1 euro per year of age per week. So a 7-year-old might get 3.50 to 7 euros weekly. The exact amount matters less than consistency. What matters most is giving them the opportunity to practice math-based decisions with real money.

What if my child struggles with math and finds money concepts frustrating?

Start with very simple tasks like counting coins or comparing two prices. Keep the stakes low and the tone playful. Tools like MathSpark can help build foundational skills with targeted worksheets before connecting those skills to money activities.

Should I use real money or play money for teaching?

Both have their place. Play money is great for younger kids who are still learning to count. But real money creates a stronger emotional connection to the math. Even small amounts, like letting a 6-year-old buy their own ice cream, make the arithmetic feel meaningful.

How do I teach about digital money when cash is disappearing?

Use a simple spreadsheet or notebook to track digital spending visually. When your child sees numbers going down after each purchase, it creates the same awareness that handling physical coins does. Some parents also use kid-friendly debit cards with apps that show transactions in real time.